Businesses looking for fast, flexible financing often turn to business lending as the most reliable way to secure the capital they need to grow, manage cash flow, or seize new market opportunities. Whether you’re launching a startup or expanding an established company, understanding the modern landscape of commercial credit— from traditional bank loans to online lines of credit— is essential to avoid costly mistakes and choose the right product for your goals. For a quick look at how a business line of credit can jump‑start a brand‑new venture, see our 2026 guide to fast, flexible funding.

Why Business Lending Remains a Cornerstone of Growth in 2026

According to the U.S. Small Business Administration’s 2026 Small Business Credit Survey, 68 % of small‑business owners reported that access to credit directly impacted their ability to hire staff, invest in technology, or increase inventory. The same report highlights that the average approved loan size grew by 12 % year‑over‑year, reflecting lenders’ growing confidence in the creditworthiness of entrepreneurs who can demonstrate strong cash‑flow projections.

Key drivers behind this trend include:

- Digital underwriting platforms that reduce approval times from weeks to hours.

- Higher availability of working capital financing tailored for seasonal businesses.

- Increased competition among fintech firms offering business line of credit products with flexible draw periods.

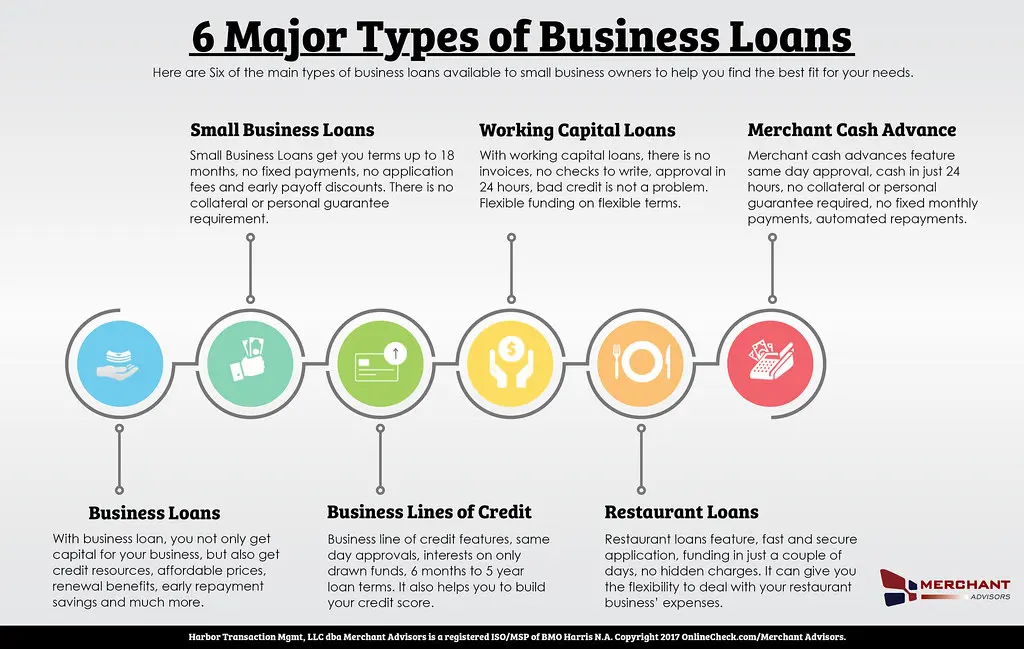

Core Types of Business Lending Available Today

1. Traditional Bank Loans

Bank loans remain the gold standard for large‑scale projects, such as purchasing real estate or major equipment. They typically feature lower interest rates—often under 6 % APR for SBA‑backed loans—but require extensive documentation and collateral.

2. Small Business Administration (SBA) Loans

The SBA’s 7(a) and 504 programs continue to dominate the “small business loan” segment. In 2025, the SBA approved $32 billion in new loans, with an average term of 10 years for working‑capital needs and up to 25 years for real‑estate financing.

3. Online Business Lines of Credit

Fintech lenders like Kabbage, OnDeck, and BlueVine dominate the commercial credit space by offering revolving credit lines ranging from $5,000 to $500,000. These products are especially attractive for businesses that need to draw funds repeatedly, such as retailers managing inventory during holiday peaks.

Our Kabbage Funding 2026 guide breaks down eligibility criteria, fee structures, and real‑world use cases.

4. Merchant Cash Advances (MCA)

While MCAs provide quick cash based on future credit‑card sales, they carry high effective APRs—often exceeding 150 %—and should be used sparingly, typically for short‑term cash‑flow gaps.

5. Equipment Financing

Specialized lenders allow businesses to lease or purchase machinery with payments spread over the asset’s useful life. This option preserves working capital while ensuring the equipment stays on the balance sheet.

How to Choose the Right Lending Product for Your Business

Matching your financing need with the appropriate product reduces costs and improves repayment success. Follow these three decision points:

- Purpose of Funds – Identify whether the capital is for growth (e.g., marketing, hiring), asset acquisition, or short‑term cash‑flow.

- Repayment Horizon – Align the loan term with cash‑flow cycles; a 12‑month line of credit suits inventory turnover, while a 10‑year loan fits real‑estate purchase.

- Cost Sensitivity – Compare APR, origination fees, and prepayment penalties across lenders.

Step‑by‑Step Blueprint to Secure Business Lending in 2026

Step 1: Clean Up Your Financials

Prepare the following documents:

- Profit & loss statements for the last 12 months (preferably audited).

- Balance sheet showing assets, liabilities, and equity.

- Bank statements reflecting cash‑flow stability.

- Tax returns (business and personal) for the past two years.

Fintech platforms often request these files during the online application, but having them organized speeds up the process.

Step 2: Calculate Your Debt‑Service Coverage Ratio (DSCR)

A DSCR above 1.25 signals to lenders that you can comfortably cover loan payments. Use the formula:

DSCR = Net Operating Income ÷ Total Debt Service

Tools like SBA’s loan calculator provide instant estimates.

Step 3: Research Lender Options

Compare at least three sources: a traditional bank, an SBA‑partner, and a reputable fintech. Look for:

- Interest rates (fixed vs. variable).

- Funding speed (same‑day, 24‑hour, or 7‑day).

- Maximum credit limit.

- Customer support and account management.

Step 4: Submit a Targeted Application

Tailor each application to the lender’s preferred metrics. For example, banks emphasize credit scores (often >680), while fintechs focus on monthly revenue trends.

Step 5: Review and Accept the Offer

Before signing, verify:

- APR and any hidden fees (origination, underwriting, or early‑repayment).

- Repayment schedule (monthly, weekly, or daily draws for lines of credit).

- Collateral requirements.

Common Mistakes Entrepreneurs Make When Pursuing Business Lending

- Over‑borrowing – Taking more credit than needed inflates debt‑service costs and reduces profitability.

- Ignoring Cash‑Flow Timing – Misaligning loan repayment dates with revenue cycles can cause liquidity crunches.

- Failing to Shop Around – Accepting the first offer often means missing out on better rates or flexible terms.

- Neglecting Credit Score Management – A single missed payment can drop a score by 30‑50 points, jeopardizing future financing.

Real‑World Case Study: From Startup to Scale‑Up with a Business Line of Credit

EcoGear, a sustainable apparel startup founded in 2024, needed $150,000 to bulk‑order organic cotton for the 2025 summer collection. Traditional banks required a 20 % down payment and a six‑month approval window, which would have delayed the launch.

Instead, EcoGear applied for a $200,000 revolving line of credit through a fintech lender, securing funds within 48 hours and paying only a 7.9 % APR. The flexible draw allowed the company to replenish inventory as sales surged, ultimately increasing revenue by 35 % YoY. This success story illustrates why many businesses now prioritize fast, flexible funding options over conventional loans.

Data Snapshot: Business Lending Landscape in 2026

| Metric | 2025 | 2026 (Projected) |

|---|---|---|

| Total approved commercial credit ($bn) | 210 | 235 |

| Average APR for SBA 7(a) loans | 5.6 % | 5.4 % |

| Fintech line of credit approval speed | 3‑5 days | 1‑2 days |

| Share of small businesses using MCAs | 12 % | 9 % |

| Average DSCR of approved borrowers | 1.30 | 1.34 |

Sources: Federal Reserve’s “Commercial Credit Survey 2025”, SBA Annual Report 2025, and industry analysis from PitchBook.

FAQs About Business Lending in 2026

What is the fastest way to obtain a business line of credit?

Fintech platforms that use automated underwriting can fund a line within 24‑48 hours, provided you meet minimum monthly revenue thresholds (often $10,000‑$15,000).

Can a startup with no credit history qualify for a loan?

Yes, many lenders consider alternative data such as payment processor history, invoicing platforms, and even social‑media engagement. A strong cash‑flow forecast can offset a thin credit file.

Are there tax implications for receiving a business loan?

Loan proceeds are not taxable income. However, interest paid on qualifying business loans is generally deductible as a business expense on your federal tax return.

How does a merchant cash advance differ from a traditional loan?

An MCA is a purchase of future sales at a fixed factor rate, resulting in a higher effective APR and daily or weekly repayments tied to card‑sale volume.

What should I watch for in loan agreements?

Key clauses include pre‑payment penalties, covenant breaches (e.g., maintaining a minimum cash balance), and the definition of “default” which may trigger immediate repayment demands.

Future Outlook: What to Expect in Business Lending Over the Next Five Years

Artificial intelligence and blockchain are set to reshape underwriting, enabling real‑time risk assessment based on transactional data. By 2030, experts from the World Bank predict that digital‑first lenders could account for over 40 % of total commercial credit volume, dramatically reducing the cost of capital for underserved markets.

Businesses that adopt robust financial management software and maintain transparent reporting will be best positioned to leverage these emerging financing avenues.

Take Action Today

If you’re ready to explore the most suitable financing route, start by assessing your cash‑flow needs and then compare at least three lenders—one traditional, one SBA‑partner, and one fintech. For a deeper dive into loan structures and cost breakdowns, our Business Loan Blueprint 2026 offers a step‑by‑step approval guide that walks you through every stage.

Remember, the right business lending strategy not only fuels growth but also safeguards your company’s financial health for the long haul.