For entrepreneurs who need immediate cash without surrendering equity, a new business line of credit is often the quickest and most flexible solution. Unlike a traditional term loan, a revolving credit line lets you draw, repay, and draw again as cash flow ebbs and flows, making it ideal for covering inventory purchases, marketing campaigns, or unexpected expenses. If you’re wondering how to qualify, what costs to expect, and which lenders offer the most competitive terms in 2026, this guide walks you through every critical step.

What Exactly Is a New Business Line of Credit?

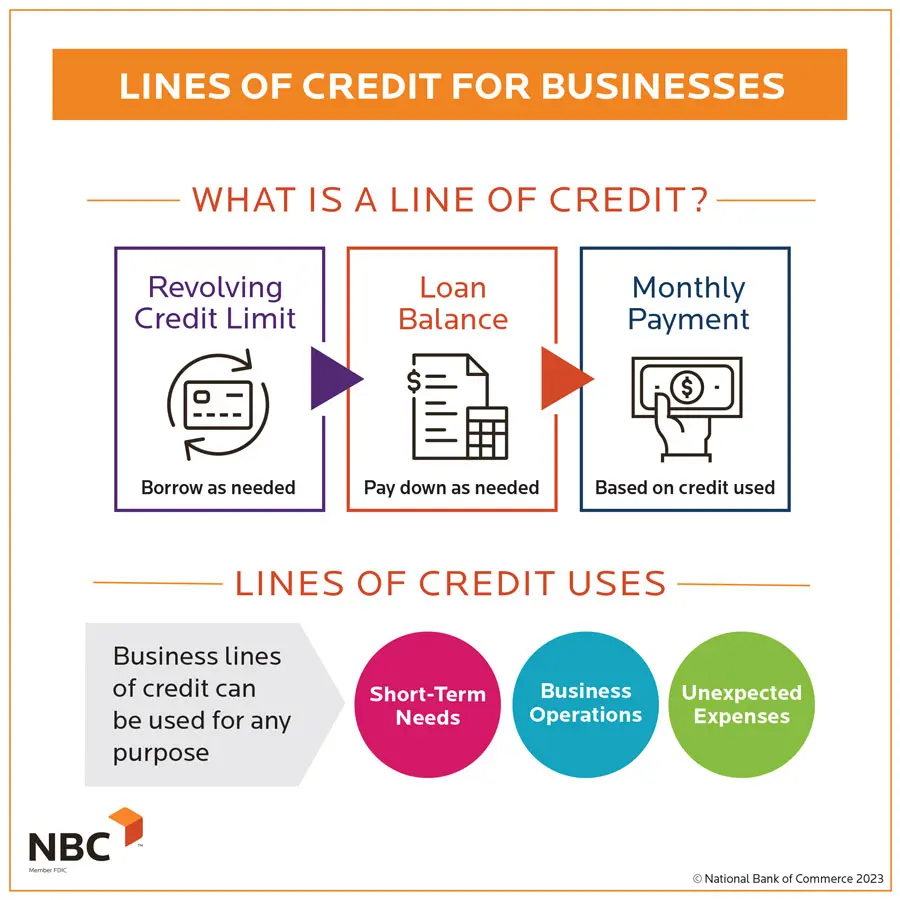

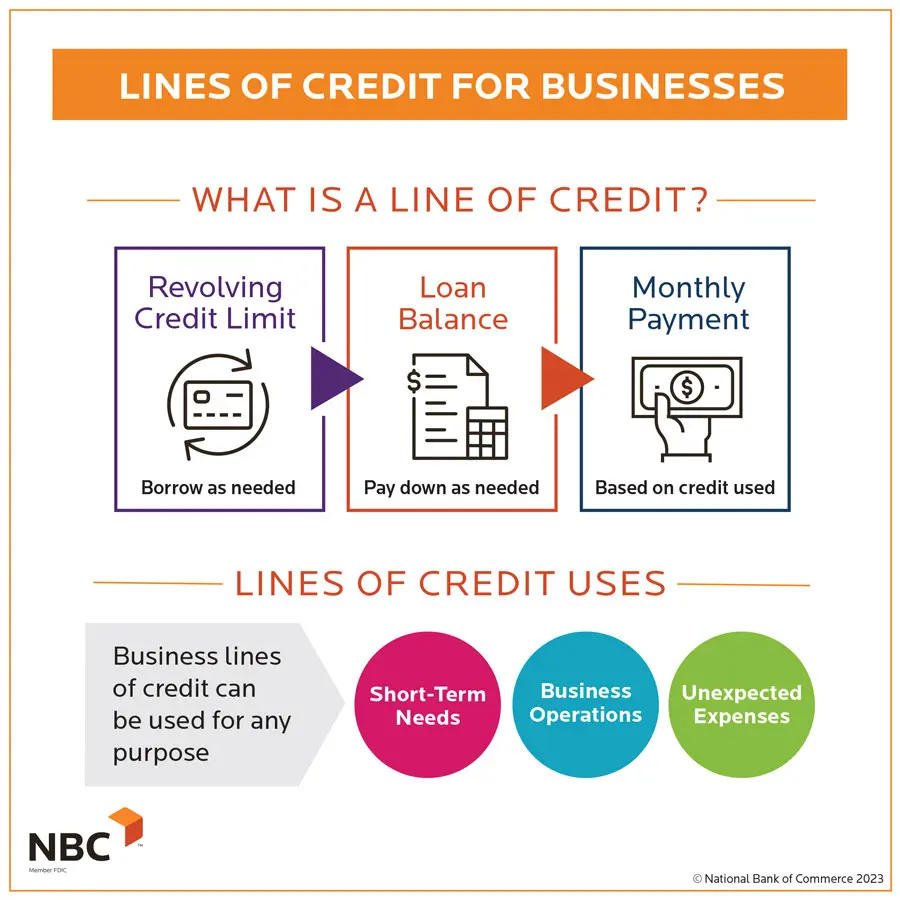

A new business line of credit (BLOC) is a pre‑approved pool of funds that a company can tap into at any time, up to a maximum limit. Think of it as a financial safety net that operates much like a credit card for businesses: you only pay interest on the amount you actually use, not on the entire credit limit.

Key characteristics include:

- Revolving nature: Once you repay the drawn amount, your credit line refreshes automatically.

- Flexible draw schedule: No fixed repayment calendar; you can withdraw whenever you need cash.

- Variable interest rates: Rates often align with the prime rate plus a margin, which can change over the life of the line.

Why Start a Credit Line When Your Business Is Still New?

Even startups face cash‑flow gaps—whether it’s buying raw materials before a first sale or scaling a marketing campaign that promises rapid growth. A new business line of credit provides:

- Working capital support without diluting ownership.

- Speed: Many lenders approve and fund within 24‑48 hours, faster than most term loans.

- Credit building: Regular, on‑time usage and repayment improve your business credit score.

According to a 2026 report by the Small Business Administration (SBA), 68 % of startups that secured a revolving credit line within their first 12 months reported smoother cash‑flow management and higher survival rates.

Eligibility Criteria – What Lenders Look For

Revenue and Cash Flow

Most lenders require a minimum of $30,000–$50,000 in annual revenue, even for a new line. However, Kabbage Funding 2026 shows that alternative fintechs may approve lines with as little as $10,000 in monthly recurring revenue if you have strong transaction data.

Credit Score

Personal and business credit scores both play a role. A personal FICO score of 680+ and a business credit score (e.g., Dun & Bradstreet) of 70+ typically unlock the most favorable rates.

Time in Business

Traditional banks still prefer at least six months of operating history, while online lenders can be more lenient, focusing on cash‑flow trends instead of the calendar age of the company.

Top Lenders Offering New Business Lines of Credit in 2026

Below is a snapshot of the most competitive options based on APR, credit limit, and approval speed.

| Lender | Maximum Credit Limit | APR Range | Funding Speed |

|---|---|---|---|

| Bank of America – Business Advantage | $250,000 | 6.99%–12.49% | 3–5 business days |

| Kabbage (American Express) | $500,000 | 8.99%–15.99% | 24–48 hours |

| BlueVine | $250,000 | 7.00%–12.00% | 24 hours |

| Fundbox | $150,000 | 8.50%–13.50% | Instant |

| Live Oak Bank | $1,000,000 | 5.75%–9.95% | 5–7 business days |

For a deeper dive into fintech‑focused credit lines, see our Kabbage Funding 2026 guide, which breaks down application nuances and hidden fees.

Step‑by‑Step Process to Secure Your Credit Line

1. Prepare Core Documentation

- Personal and business tax returns (last 2 years).

- Bank statements (last 3 months).

- Profit‑and‑loss statements or a cash‑flow forecast.

- Legal documents – Articles of Incorporation, EIN confirmation.

2. Choose the Right Lender

Match your business profile with a lender’s strengths. If you need ultra‑fast funding, fintechs like BlueVine excel. For larger limits and lower APR, traditional banks such as Live Oak Bank are preferable.

3. Complete the Online Application

Most platforms use automated underwriting powered by AI. Expect to answer questions about monthly recurring revenue, average invoice size, and your intended use of the line (e.g., inventory, payroll, marketing).

4. Review the Offer

Pay attention to:

- Draw fee – a one‑time charge (typically 1%–3% of the credit limit).

- Monthly maintenance fee.

- Early‑repayment penalties (rare, but some lenders impose them).

5. Accept and Set Up Access

After acceptance, you’ll receive a virtual credit card or a draw portal. Most lenders allow you to integrate the line directly with your business checking account, automating the draw‑and‑repay cycle.

Common Pitfalls to Avoid

- Using the line for non‑business expenses: This can jeopardize your credit limit and lead to higher scrutiny.

- Ignoring the variable rate clause: Rate hikes can increase monthly interest costs dramatically; set a budget that accounts for a 2%‑3% increase.

- Failing to make minimum payments: Even if you haven’t drawn funds, most lenders require a small monthly fee to keep the line active.

- Over‑reliance on credit: Treat the line as a supplement, not a primary financing source; diversify with term loans or equity when possible.

Real‑World Example: How a Startup Used a Credit Line to Scale

Eco‑Gear, a sustainable apparel brand founded in 2025, faced a cash‑flow crunch when a large retailer placed a $150,000 order for a limited‑edition line. The founders drew $80,000 from a $200,000 credit line with BlueVine, used the funds to purchase organic cotton, and fulfilled the order within 30 days. The sale generated $250,000 in revenue, allowing them to repay the line in full within two months and avoid equity dilution.

This case mirrors findings from a 2026 SBA market study, which reported that businesses that combined a revolving credit line with strategic inventory financing grew revenue 23 % faster than those relying solely on term loans.

Comparing a Line of Credit to Other Funding Options

| Funding Type | Typical Use | Repayment Structure | Cost (APR) |

|---|---|---|---|

| Business Line of Credit | Working capital, short‑term projects | Revolving, interest‑only on drawn amount | 6.99%–15.99% |

| Term Loan | Equipment, expansion | Fixed monthly payments | 5.75%–12.50% |

| No‑Doc Business Loan | Quick cash, minimal paperwork | Fixed term, higher fees | 12%–25% |

| Invoice Financing | Unpaid invoices | Fee per invoice (1%–3%) | Varies |

For a concise overview of no‑doc loans, see our No Doc Business Loan 2026 guide, which explains why a line of credit often remains the more cost‑effective choice for ongoing liquidity.

Frequently Asked Questions

Can I get a line of credit if I have no revenue yet?

Some fintech lenders offer “pre‑revenue” credit lines based on projected cash flow, but rates are higher (up to 18%). Traditional banks usually require at least six months of revenue.

How does a credit line affect my business credit score?

Responsible usage—keeping utilization below 30% and making timely payments—boosts your score. Missed payments can lower it as quickly as a missed loan payment.

What is the difference between a secured and unsecured line?

Secured lines require collateral (e.g., equipment, real estate) and often feature lower APRs. Unsecured lines rely solely on creditworthiness and usually have higher rates and lower limits.

Is there a tax advantage to using a line of credit?

Interest paid on a business line of credit is generally tax‑deductible as a business expense, similar to interest on a term loan. Consult a CPA for exact calculations.

Can I increase my credit limit later?

Yes. After six months of consistent repayment, most lenders will review your usage and may raise the limit without a new application.

Future Outlook: What to Expect in 2027 and Beyond

AI‑driven underwriting is set to further shrink approval times, with some platforms promising instant credit decisions based on real‑time transaction data. Additionally, regulatory changes announced by the Federal Reserve in late 2026 aim to increase transparency around variable‑rate disclosures, which will help borrowers better anticipate cost fluctuations.

Staying informed about these trends will ensure you choose the most cost‑effective, flexible financing as your business evolves.

Bottom Line – Is a New Business Line of Credit Right for You?

If you need a nimble funding source that grows with your sales cycle, a new business line of credit offers unmatched flexibility, rapid access, and the ability to preserve equity. By assessing your cash‑flow patterns, selecting the right lender, and managing the line responsibly, you can turn short‑term gaps into long‑term growth opportunities. For a broader perspective on securing fast, flexible funding, explore our Business Lending 2026 ultimate guide, which covers everything from lines of credit to term loans and beyond.

Ready to start? Gather your documents, compare offers, and apply today—your next growth milestone could be just a draw away.