Getting a business line of credit for a new business is often the quickest way to secure the working capital needed to cover inventory, marketing or unexpected cash‑flow gaps, and the process is surprisingly straightforward once you know the eligibility criteria and the best lenders for startups. If you’re launching a venture in 2026, understanding revolving credit options can give you the flexibility that a traditional term loan can’t, and you’ll be able to draw only what you need, when you need it.

What Exactly Is a Business Line of Credit?

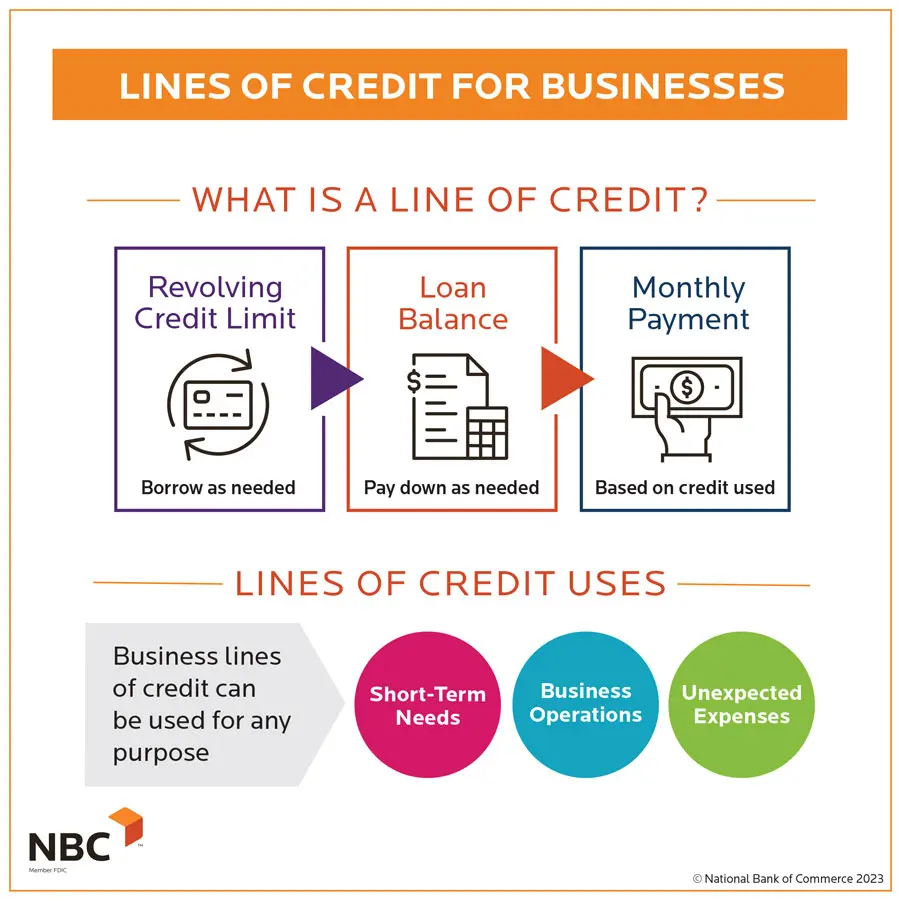

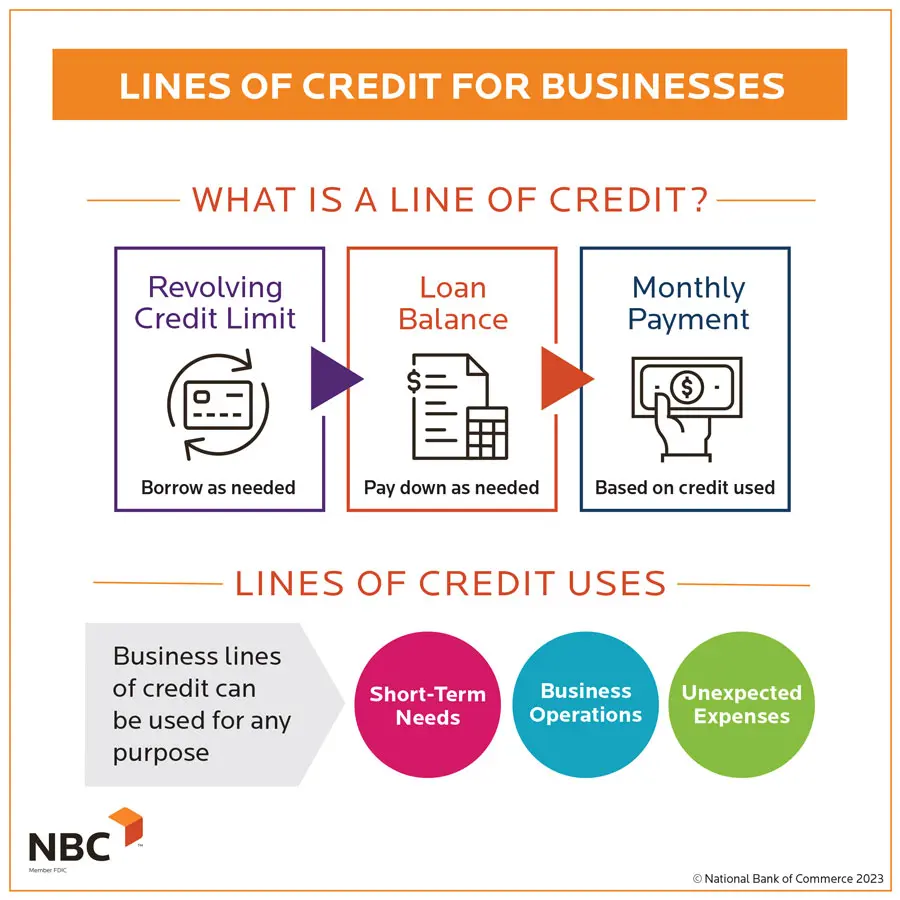

A business line of credit (BLOC) is a revolving loan facility that lets you borrow up to a pre‑approved limit, repay the amount, and borrow again without reapplying. Unlike a term loan, where you receive a lump sum and make fixed payments, a BLOC functions much like a credit card for your company: you pay interest only on the amount you draw, and you can use the funds repeatedly as long as you stay within the limit.

Why New Businesses Prefer a Line of Credit Over Other Startup Financing Options

- Flexibility: You can tap the credit line for inventory purchases one month and for a marketing campaign the next.

- Cost Efficiency: Interest accrues only on the amount drawn, unlike a term loan where you pay interest on the full principal.

- Speed: Once approved, funds are usually available within 24–48 hours, which is crucial for fast‑moving markets.

- Credit Building: Regular, on‑time repayments can improve your business credit score, opening doors to larger financing later.

Eligibility: What Lenders Look for in a New Business

While each lender has its own underwriting model, most assess the following key factors:

Revenue and Cash Flow

Even startups with limited history can qualify if they demonstrate consistent monthly cash inflow. According to a U.S. Small Business Administration (SBA) 2025 report, 68 % of approved BLOCs for businesses less than 12 months old required a minimum monthly revenue of $15,000.

Personal Credit Score

Because new businesses often lack an established credit file, lenders rely heavily on the owner’s personal credit. A score of 680 or higher typically places you in the “prime” tier, unlocking lower interest rates.

Business Plan and Use of Funds

A concise plan outlining how the line will be used—whether for inventory, payroll, or marketing—helps lenders gauge risk. Including projected cash‑flow statements strengthens the application.

Industry and Market Trends

Lenders favor sectors with strong growth trajectories. In 2026, e‑commerce, health‑tech, and renewable energy saw the highest approval rates for revolving credit, according to data from Federal Reserve Bank.

Top Providers of Business Lines of Credit in 2026

Below are the most reputable lenders offering flexible credit lines for startups, based on interest rates, approval speed, and customer satisfaction.

Kabbage (now part of American Express)

Kabbage remains a favorite for rapid funding. The Kabbage Funding 2026 guide notes that approved borrowers can access up to $250,000 with a simple online application and receive funds within a day. Rates range from 7.99 % to 24.99 % APR, depending on creditworthiness.

BlueVine

BlueVine offers lines from $5,000 to $250,000 with an average APR of 8.5 % for prime borrowers. Their platform integrates directly with accounting software, making draw‑downs and repayments seamless.

Fundbox

Fundbox specializes in short‑term revolving credit up to $150,000, ideal for businesses that need quick working capital. Their proprietary AI evaluates cash‑flow data rather than relying solely on credit scores.

Traditional Banks (e.g., Chase, Wells Fargo)

While banks often have stricter criteria, they provide the lowest rates for qualified startups—sometimes as low as 5.5 % APR. However, the application process can take 2–4 weeks.

Step‑by‑Step Guide to Securing a Business Line of Credit

- Gather Your Documents

- Personal and business tax returns (last two years)

- Bank statements (3–6 months)

- Business plan with cash‑flow projections

- Legal documents (EIN, articles of incorporation)

- Check Your Personal Credit Score – Use a free service like AnnualCreditReport.com and dispute any inaccuracies before applying.

- Compare Lender Offers – Look at APR, draw‑down fees, and repayment terms. Tools like NerdWallet provide side‑by‑side comparisons.

- Submit an Online Application – Most modern lenders (Kabbage, BlueVine) require just a few clicks. Upload documents securely and answer the use‑of‑funds questions.

- Review the Credit Agreement – Pay attention to draw‑down limits, interest accrual methods, and any hidden fees (e.g., inactivity fees).

- Activate the Line and Manage Draw‑downs – Use the lender’s portal or integrate with your accounting software to pull funds as needed.

- Make Timely Payments – Set up automatic payments to avoid late fees and to improve your credit profile.

Common Pitfalls and How to Avoid Them

Over‑borrowing

Because a line of credit is flexible, it’s easy to draw more than you can afford to repay. Keep a utilization ratio below 30 % of the limit to maintain a healthy credit score.

Ignoring Fees

Some lenders charge a monthly maintenance fee (often $15‑$30) even if you don’t draw funds. Read the fine print to factor these costs into your budgeting.

Poor Cash‑Flow Management

Using a line for short‑term fixes without addressing underlying cash‑flow problems can lead to a debt spiral. Pair the credit line with robust cash‑flow forecasting.

Real‑World Case Study: From Zero to $100K Revenue in Six Months

Emma, founder of a boutique organic skincare brand, launched her e‑commerce store in January 2026. She needed inventory for a new product line but had only $12,000 in seed capital. By securing a $50,000 line of credit from BlueVine, she was able to purchase raw materials in bulk, saving 15 % on costs. Within three months, her sales surged to $45,000 per month, and she repaid $30,000 of the line, keeping the remaining balance as a safety net for seasonal demand spikes. Emma also leveraged a best website builder for small business to optimize her site, which contributed to a 25 % increase in conversion rates.

Data & Statistics: The State of Business Lines of Credit in 2026

- According to the Federal Reserve’s 2026 Small Business Credit Survey, 42 % of businesses under two years old used a revolving credit line as their primary financing source.

- The average APR for startup lines dropped to 9.2 % in 2026, down from 11.5 % in 2024, reflecting increased competition among fintech lenders.

- Utilization rates among new businesses averaged 27 % of approved limits, indicating prudent borrowing habits.

- Failure rates for businesses that relied solely on term loans without a supplemental line of credit were 18 % higher, per a study by National Bureau of Economic Research.

FAQ: Quick Answers to Common Questions

Can a startup with no revenue get a line of credit?

Yes, but the options are limited. Fintech lenders like Fundbox may approve based on projected cash flow and personal credit, while traditional banks usually require at least six months of revenue.

How long does the approval process take?

Fintech platforms typically approve within 24–48 hours. Banks can take 2–4 weeks due to more extensive underwriting.

What is the difference between a secured and unsecured line of credit?

Secured lines require collateral (e.g., equipment, inventory) and often come with lower rates. Unsecured lines rely solely on creditworthiness and have higher APRs.

Do I pay interest on the entire credit limit?

No. Interest accrues only on the amount you actually draw. Unused portions remain interest‑free.

Can I increase my credit limit later?

Most lenders allow limit increases after 6–12 months of on‑time payments and demonstrated usage.

Comparing a Business Line of Credit with a Traditional Business Loan

If you’re still undecided, consider the Business Loan Blueprint 2026. While term loans provide a fixed lump sum ideal for large, one‑time investments like equipment purchases, a line of credit offers ongoing flexibility for day‑to‑day operations. The choice depends on your cash‑flow pattern, growth stage, and the predictability of expenses.

Final Thoughts: Making the Right Choice for Your New Business

A business line of credit can be a powerful tool for entrepreneurs who need agile, cost‑effective financing. By understanding eligibility, selecting a reputable lender, and managing draw‑downs responsibly, you can keep your startup’s cash flow healthy and position it for sustainable growth. Remember to compare offers, watch for hidden fees, and use the credit line as a strategic partner—not a crutch.